by Wang Kai

One month after Donald Trump took office, U.S. inflation surged to 3% for the first time since June, marking it as one of the administration’s most pressing economic challenges.

However, the root causes of this inflationary pressure go deeper than short-term policy changes. A recent report by KTrade Securities highlights that amidst upward inflation risks that stemmed from fiscal deficit, fueled by exorbitant debt, and complicated by rising tariffs, the U.S. economy is slowing down and showing signs of recession. It warns that adopting an isolationist approach—focusing on domestic priorities while disengaging from global trade—will not address the structural issues facing the economy. Instead, it could accelerate the very problems it aims to prevent.

Inflation taking hold

The U.S. national debt has ballooned to 123% of its GDP, a level that raises serious concerns about fiscal sustainability. With such a high debt burden, monetary policy (controlled by the Federal Reserve) is taking a backseat to fiscal policy (government spending and taxation). This shift is expected to fuel inflation, especially as the Fed may be forced to monetize the deficit—essentially printing money to cover government shortfalls.

“We believe fiscal deficits rather than bank lending is the root cause of inflationary pressures in the U.S. economy. As such, the Fed’s ability to manage inflation via interest rates may not be effective,” according to the report.

The Congressional Budget Office (CBO) in its latest Outlook report alludes to the deficit problem where its forecasts mandatory and net interest costs to average 75% of total government spending in the decade through 2035, putting a question mark on the effectiveness of the efforts by the Department of Government Efficiency (DOGE) to cut discretionary spending.

Muhammad Aimen, an investment analyst at KTrade Securities, notes, “The mandatory expenditure includes social security, medicare, defense spending, and net interest costs. Very recently, we’ve seen net interest costs are actually the second biggest item.”

Adding to the fiscal pressure, an extension of the Trump Jobs and Tax Cuts Act, set to expire in 2025/26, could add another $4 trillion to the national debt over the next decade.

“Whenever a nation exceeds 100% debt, they almost always inflate away the debt, which means that the U.S. will probably face ultra long period of financial repression, where inflation outpaces economic growth,” Muhammad Aimen said.

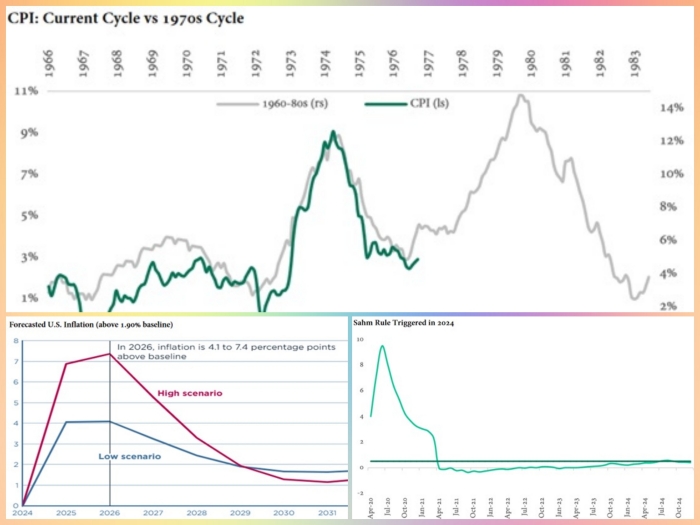

Historical comparisons also suggest that inflation could re-accelerate. The current Consumer Price Index (CPI) cycle bears similarities to the high inflation period of the 1970s, raising concerns about a potential repeat of that era’s economic struggles.

The market shares concerns about U.S. fiscal sustainability and the possibility of inflation reaccelerating, as evidenced in the fact that yields on the U.S. 10-year bond climbed to the highest level since 2023 in January, indicating pessimism towards the economy in near term, the report noted.

Tariffs: Adding Fuel to the Fire

The announced tariffs on China, Mexico and Canada – the 3 largest trade partners of the U.S. – risk stoking inflation by curbing access to cheap labor and goods. Deportation of immigrants could also lead to higher domestic prices, considering around 15% of construction, manufacturing and agriculture workers in the U.S. are immigrants.

A recent study by the Peterson Institute for International Economics (PIIE) estimates that tariffs and immigration restrictions could push U.S. inflation to between 6.0% and 9.3%, significantly higher than the baseline estimate of 1.90%. Over time, this could lead to a cumulative price increase of 20% to 28% for U.S. consumers by 2028.

PIIE forecasted U.S. inflation. Graph by KTrade Securities.

“Even if these tariffs do bring some manufacturing back on shore, will these industries be competitive in the global market?” Muhammad Aimen questioned. “In other markets, Chinese manufacturers will continue to gain share, and the U.S. runs the risk of being shut out.”

Eventually, the cost of disrupted supply chains caused by tariffs will be borne by American consumers. Analysis by U.S. Tax Policy Center shows that an average American family will have to increase their spending by about $1,350 to $3,900 per year as a result of tariffs.

Tipping Point for Recession Has Arrived

Despite of a strong Dollar in sight thanks to its status as a global reserve currency, its relative advantages from the expected devaluation of other currencies in response to tariffs, and demand from dollar-denominated debt, skepticism about U.S. economic sustainability sweeps across investors.

Global market players have turned to alternative assets. Gold and bitcoin, often seen as hedges against inflation and currency devaluation, have posted remarkable returns in 2023 and 2024. Central banks reemerge as the largest net buyers of gold. In 2024 alone, central banks acquired 1,045 tonnes of gold – marking 3 consecutive years with over 1,000 tonnes purchased. Bitcoin ETFs saw $4.5bn net inflows last month with assets under management (AUM) officially surpassing $125bn for the first time in history.

Amid diminishing interest in the hegemonic currency, attention is also turning to key indicators that signal broader economic health—or distress. The CBO has forecast a decline in real GDP growth to 1.90% in FY25, and below trend growth for the decade through 2035.

Historically, a reliable real-time indicator of recession has been the Sahm Rules, which is triggered when the 3-month moving average of the unemployment rate rises by 0.5 percentage points or more relative to its lowest point in the previous 12 months. It has successfully been triggered at the onset of every U.S. recession in the last 50 years.

In August last year, Sahm Rules was triggered, signaling a weakening labor market—a precursor to broader economic downturns.

Sahm Rule Triggered in 2024. Graph by KTrade Securities.

Since May 2023 when unemployment hit 4% (the highest since February 2022), it has remained elevated. Wage growth has failed to keep pace with rising costs, leading to record-high credit card debt exceeding $1 trillion. Moody’s Analytics reports that the bottom third of U.S. consumers have a savings rate of zero, effectively living paycheck to paycheck. A Bank of America study found that 30% of American households spend at least 90% of their disposable income on essential expenses.

Delinquency rates on credit card debt are at their highest since 2011. Credit card companies wrote off $46bn in “seriously delinquent loan” balance in June last year, a 50% y-o-y increase and the highest level since the 2008 crisis. Commercial Mortgage Backed Security (CMBS) loan delinquency as of the end of 2024 roses 41% y-o-y, with office building delinquencies increasing 90% y-o-y.

“Higher unemployment means weaker tax revenue, compounding the deficit problem. An aging population adds to entitlement costs. Without a course correction, a debt spiral is a real possibility,” the report warns. (***